TENTH PELICE LIVES UP TO BILLING IN ATLANTA

Known as “the last conference in the world,” PELICE provides boost of enthusiasm for all segments of the panel industry.

ATLANTA, Ga.

ATLANTA, Ga.

Forty-one speakers, 470 registrants and 95 exhibitors contributed to the 10th Panel & Engineered Lumber International Conference & Expo (PELICE) held April 16-17 at the Omni Atlanta Hotel at Centennial Park.

The event, which is co-hosted by Panel World magazine and Georgia Research Institute, is held every other year, with the first one occurring in 2008. That this was number 10 was an ongoing discussion, including the recognition of 18 exhibitor companies that have participated in all 10.

During the opening session, PELICE Co-Chairman and Panel World Editor-in-Chief Rich Donnell recognized Co-Chairman and GRI President Fred Kurpiel as conceiving the idea of PELICE and approaching Donnell and Panel World for a partnership back in 2006.

Twenty-five producer companies sent management personnel to soak in the non-stop rush of information and technologies, and the event began with speeches from producer executives.

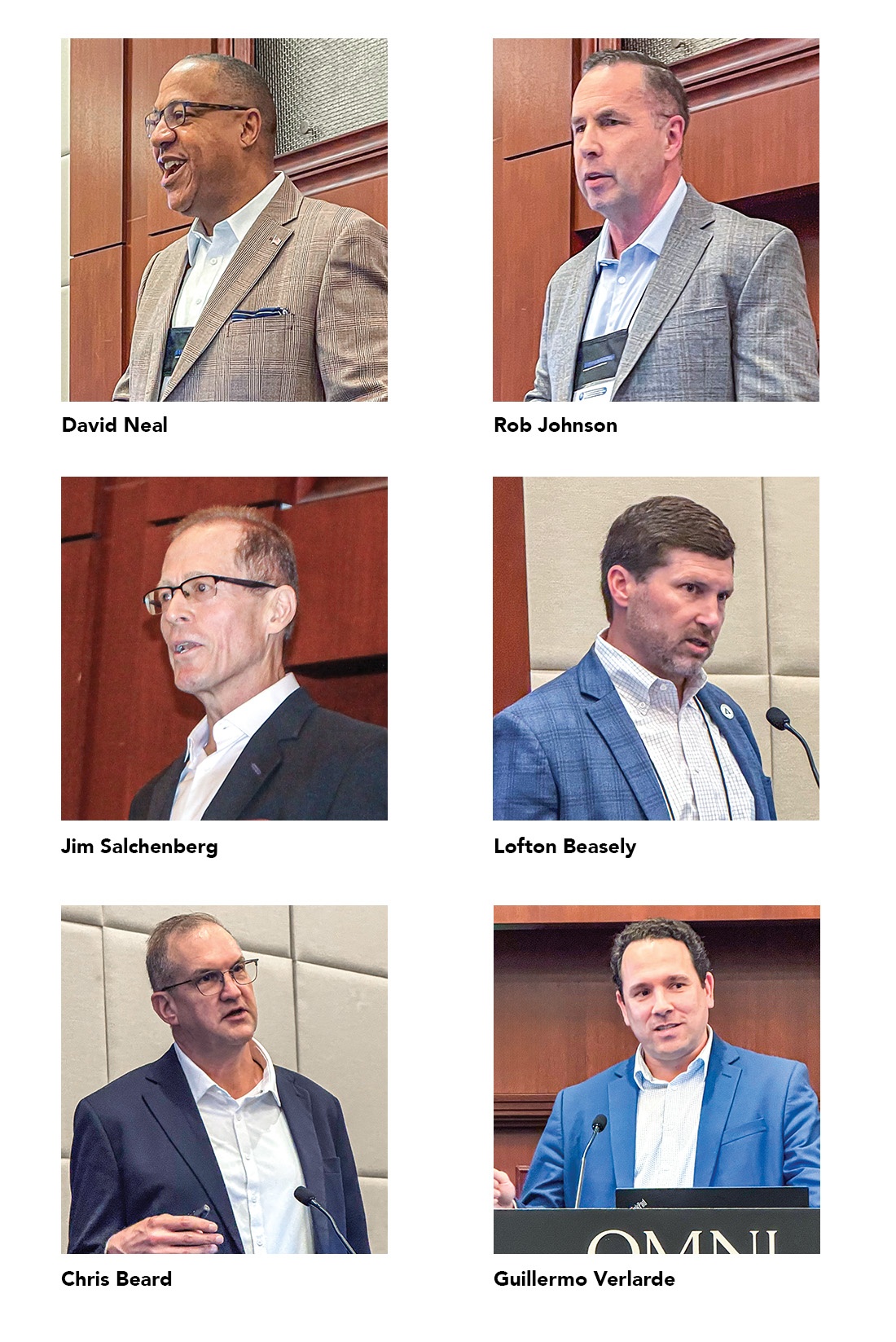

Three first morning keynote speakers addressed a full house in the Grand Ballroom North, leading off with David Neal, Vice President of Building Products at Georgia-Pacific; followed by Rob Johnson, Senior Vice-President of Manufacturing Operations at Boise Cascade; and Jim Salchenberg, Director of Strategic Projects at Roseburg.

A very active contributor himself to developments in Atlanta, Neal addressed GP’s longstanding role in the community and cultural affairs. He emphasized the importance of employee growth through a combination of in-house guidance and cultural awareness, leading to the building of relationships and trust in business and outside of business.

A very active contributor himself to developments in Atlanta, Neal addressed GP’s longstanding role in the community and cultural affairs. He emphasized the importance of employee growth through a combination of in-house guidance and cultural awareness, leading to the building of relationships and trust in business and outside of business.

Neal, who has held numerous leadership roles at GP and started there in 1997 as a quality resource manager, focused on three GP people who have excelled with those principles, including Curley Dossman, President Community Programs, who leads GP’s charitable giving program and oversees the company’s community affairs efforts; along with Soy Sharjary, Vice President of Finance Building Products, who began with GP in 2003 as a lab technician; and Mark Atkins, Senior Vice President, Strategic Accounts.

Neal pointed to the three men and to GP overall as intertwining this model of community relationships and the on-the-ground betterment of the lives and awareness of the underprivileged, with building on efforts to not only establish partnerships and provide products to customers but to evolve with customers and provide new opportunities and capabilities that meet the changing needs of these “preferred partners.”

Boise Cascade’s Johnson spoke on the perhaps historically-based misimpressions of what Boise has truly evolved into today—one of the largest wholesale distributors of building products in the U.S., and one of the largest producers of LVL, I-Joist and plywood in North America with 18 manufacturing locations.

He said the company has resisted the urge to diversify its portfolio significantly, opting to remain with its expertise in an integrated framework regardless of market conditions. And he added that the distribution element stabilizes extreme swings in financial performance, providing margin consistency across market bounces.

More specifically to wood products, Johnson stated, “We are an EWP focused business. Our veneer mills also produce plywood, but we consider it a byproduct of strength rated veneer production.”

He said the business is geared to self-sufficiency of supply in veneer production—95% self-sustained in veneer in the West and 100% in the Southeast—supported by continued modernization of facilities.

Why EWP? Johnson said builders demand EWP in new home construction as a superior solution in consistency of design and building practice while reducing waste.

Only days after Roseburg announced it was resuming construction of a new MDF plant in Dillard, Ore., that project and others as part of a billion dollar capital investment program was addressed by Jim Salchenberg, Director of Strategic Projects at Roseburg.

Salchenberg noted that a stack of a billion one-dollar bills reaches higher than where commercial planes fly, and he added that the legacy of “big” at Roseburg was started by founder Kenneth Ford. Salchenberg said Roseburg approved more than 400 capital projects totaling more than $1.1 billion from 2021-2024. He said the new MDF mill in Dillard is planned for startup in late 2028, and is being built where the long-running now shuttered particleboard mill was.

Roseburg delivered the capital portfolio of projects within 3% of investment goals despite post-Covid challenges, according to Salchenberg, who provided three tips for budget control: Own the budget (manage every sub-cost within the budget); protect the scope relentlessly; and never accept “it takes what it takes, and it costs what it costs.”

Another keynote speaker from the producer sector, who spoke on the second morning of PELICE, was Lofton Beasley, Product Manager at Weyerhaeuser. He spoke on driving strategic growth for engineered wood products and innovative approaches to expanding engineered wood markets.

Beasley said there is a strategic urgency behind accelerating growth in EWP, emphasizing that structural changes in the construction industry are shifting demand away from traditional commodity products toward engineered, system-based solutions that deliver speed, predictability, and performance. Customers—ranging from builders to designers—are increasingly focused on solutions that mitigate labor shortages, reduce variability, and shorten build cycles.

“These forces are structural, not cyclical, meaning they will persist regardless of short-term market fluctuations,” he said, adding that the opportunity for Weyerhaeuser is to improve its long-term earnings profile by leaning into differentiated engineered products that are less exposed to commodity price volatility.

“The key executive message is that while housing markets may be volatile in the near term, strategic action must be taken now to position EWP as a durable growth engine that delivers sustained value creation across market cycles.”

Building codes and standards increasingly favor engineered solutions due to their structural performance and reliability, Beasley added. At the same time, persistent labor constraints and risk aversion among builders are accelerating the adoption of repeatable, prefabricated, and system-based construction approaches.

Weyerhaeuser is adding to its engineered wood capacity in North America with the ongoing construction of a TimberStrand facility in Monticello, Ark. The new facility addresses underserved and growing market for TimberStrand in the U.S. South, Beasley said, and its enable conversion of lower quality southern logs and forest byproducts into a higher value EWP product, with 80% of raw material sourcing expected to come from company fee timberlands. The new facility will add 10 million cubic feet of products capacity and increase total company EWP capacity by 24%.

A post-lunch keynoter was Chris Beard, Vice President Building Products Research at John Burns Research and Consulting, who addressed the drivers impacting wood panel usage in housing.

Beard said building product spending will be $485 billion in 2026, down 0.6%, but while the market is essentially flat, it’s not necessarily static, as the mix of demand continues to shift.

He said new construction is “the near-term drag,” noting that the gap between unsold single family homes under construction and those completed remains large, with completed homes representing 27% of total inventory. He added that March single-family new home starts per community fell to the lowest March level in six years. Meanwhile, residential improvements spending continues to become more important, and is basically equal to the combination of new single-family homes and new multifamily homes.

Beard said the median U.S. home is now 44 years old, and new builds in the last 20 years represent just 16% of total stock. Homes built in the early 2000s construction boom now need significant upgrade.

While Beard expects a decline in single-family starts in 2026 of 2%, he does forecast a recovery in 2027, 2028 and 2029 of positive 4%, 3% and 4%, respectively. Multifamily will also decline in 2026 by 9%, followed by recovery of 8%, 7% and 7%.

He added that custom homebuilding starts have shown an uptick over the past few years, resulting in an increase to average home sizes.

The real opportunity is in repair and remodeling, and one reason is that tax refunds this season are expected to be significantly larger than usual, providing a tailwind to remodeling. He says the number of homeowners in their peak remodeling years will grow slowly through 2028.

Also, home equity levels are near all-time high, far exceeding the peak of the 2000s housing bubble. Home equity-based financing is most often used for remodeling projects.

Another factor is “the disaster repair wild card.” Damages from billion dollar events are becoming more frequent over time.

Guillermo Velarde, principal at AFRY Management Consulting, addressed the big picture for structural and composite panel markets.

With regard to OSB, he said capacity will increase in North America, but new capacities will put installed capacity at risk, all the while dependent on construction.

He said the ongoing substitution pressure from OSB, driven by cost advantages and better technical properties, is limited future demand growth of softwood plywood.

He noted particleboard is a very consolidated market in North America. Competitive exports from contemporary, large-scale European particleboard factories are increasingly challenging the older and smaller mills in North America. But total market potential surpasses installed capacity.

In MDF, new announced capacity is expected to be competitive against imports due to high efficiency and competitive raw material costs.

AFRY recommends operational improvement of the plant, including process improvements, variable cost and energy savings, and if necessary organizational changes. It also recommends logistics and Supply Chain Management improvements, and profitability actions; and changes in raw material sourcing strategies on one end and product portfolio diversification on the other, and an overall review an enhancement of innovation strategy.

There was much more during PELICE, including major discussions on Artificial Intelligence, Catastrophe Management, Wood Fiber, Project Develoment, Production Improvements, Additives & Applications, Veneer & Plywood Manufacturing, Fire and Safety Technologies, Mass Timber, and Energy & Emissions.

Latest News

Kirk Blanchette To Lead Huber Engineered Wood

Kirk Blanchette To Lead Huber Engineered WoodHuber Engineered Woods (HEW) has announced that Kirk Blanchette will become President of HEW, succeeding Brian Carlson, who is retiring as of July 1. Blanchette will bring more than 25 years of experience in finance,...

Walmart Home Office Installs Mercer CLT, Glulam

Walmart Home Office Installs Mercer CLT, Glulam Mercer Mass Timber (MMT), a manufacturer of timber building materials and a subsidiary of Mercer International Inc., has announced the completion of a key role in the construction of Walmart’s new Home Office in...

TimberHP Expects Long-Term Success

TimberHP Expects Long-Term SuccessTimberHP, a Maine-based manufacturer of wood fiber insulation, announced that it has filed a voluntary, pre-negotiated Chapter 11 plan of reorganization in the U.S. Bankruptcy Court for the District of Delaware. The plan, according to...

Find Us On Social

Newsletter

The monthly Panel World Industry Newsletter reaches over 3,000 who represent primary panel production operations.

Subscribe/Renew

Panel World is delivered six times per year to North American and international professionals, who represent primary panel production operations. Subscriptions are FREE to qualified individuals.

Advertise

Complete the online form so we can direct you to the appropriate Sales Representative. Contact us today!